The Bounce Changes Nothing

Markets bounced, but little has really changed. We remain trapped in a regime defined by extreme volatility, violent rotations and increasingly unstable market structure. The easy part of the bounce appears to be over...

Now what?SPX bounced on the 50 day MA and is now back to the 50% of the big down candle. The easy part of the bounce is over, and given the fact we are trading in the middle of the range, we see little short term edge.

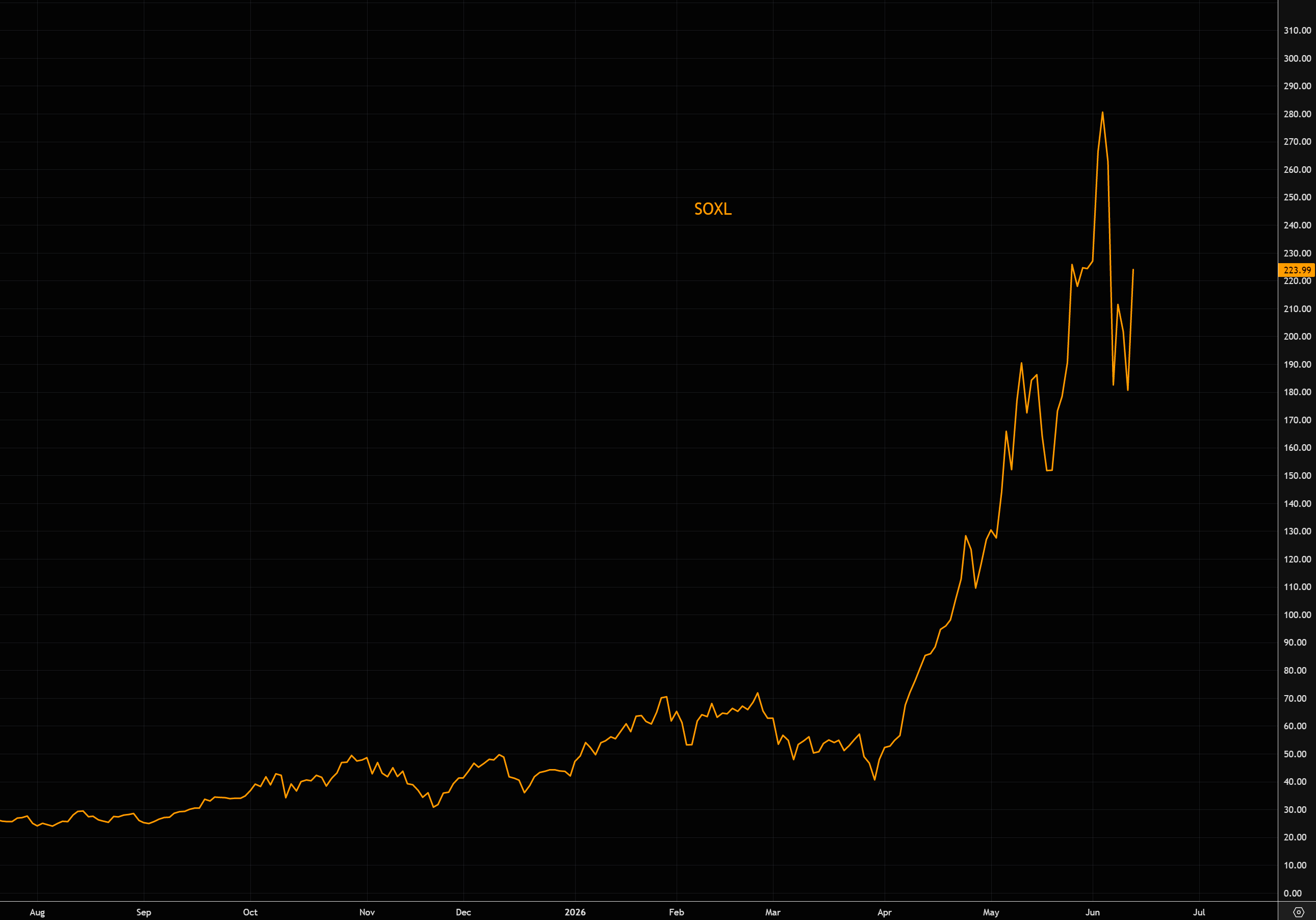

Easier said that done lately. We are basically unchanged since late May, but moves, both ways, have been extreme. Chart looks like a small cap stock, but is actually showing the biggest theme around, SOX.

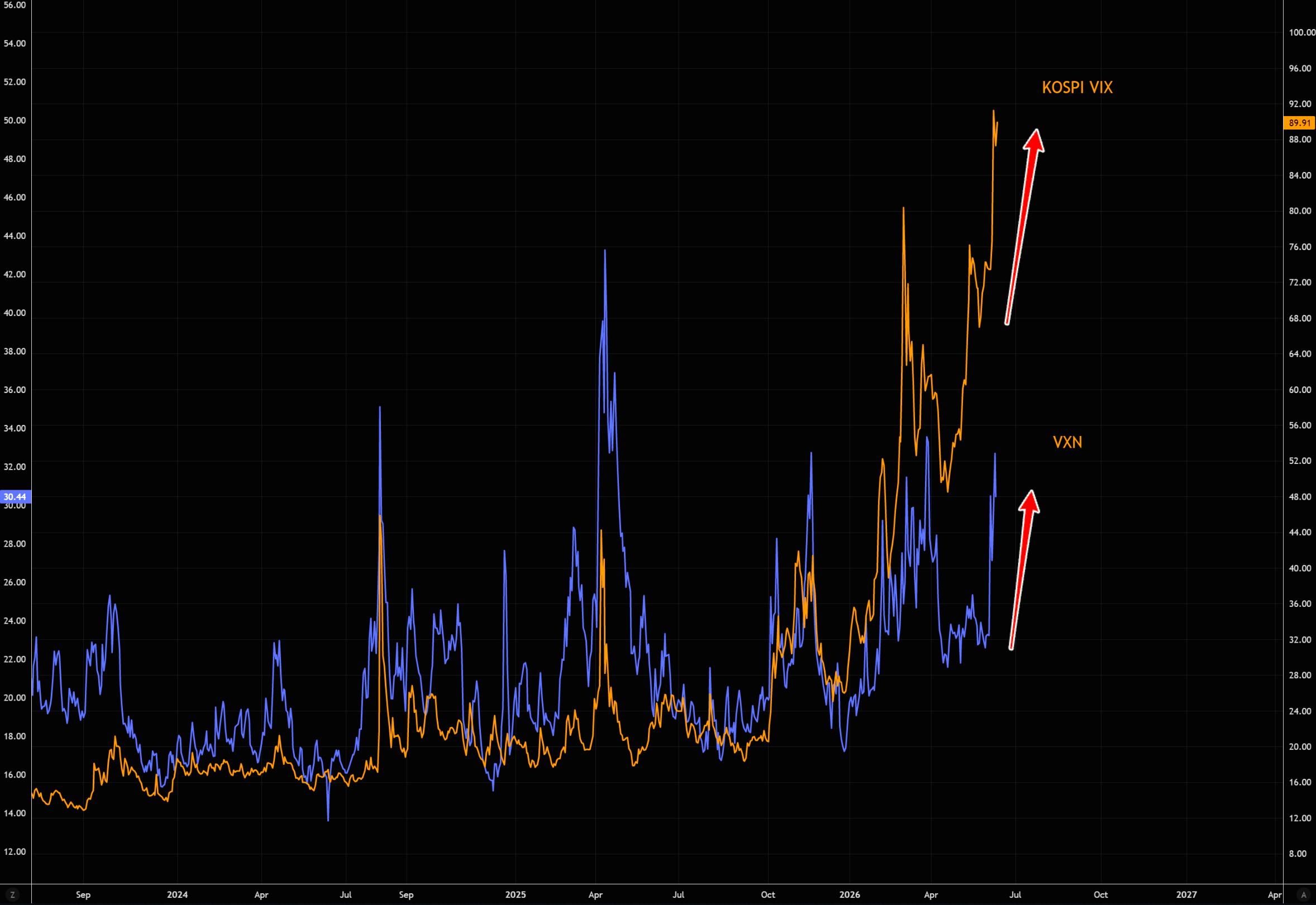

The world's fifth/sixth-largest equity market is trading with a "VIX" near 90. That is an extraordinary level of volatility and a sign of just how unstable the environment has become.

NASDAQ volatility is also elevated, but it pales in comparison to what is happening in Korea. The broader point is that technology volatility has become so extreme that managing risk in any meaningful way is increasingly difficult.

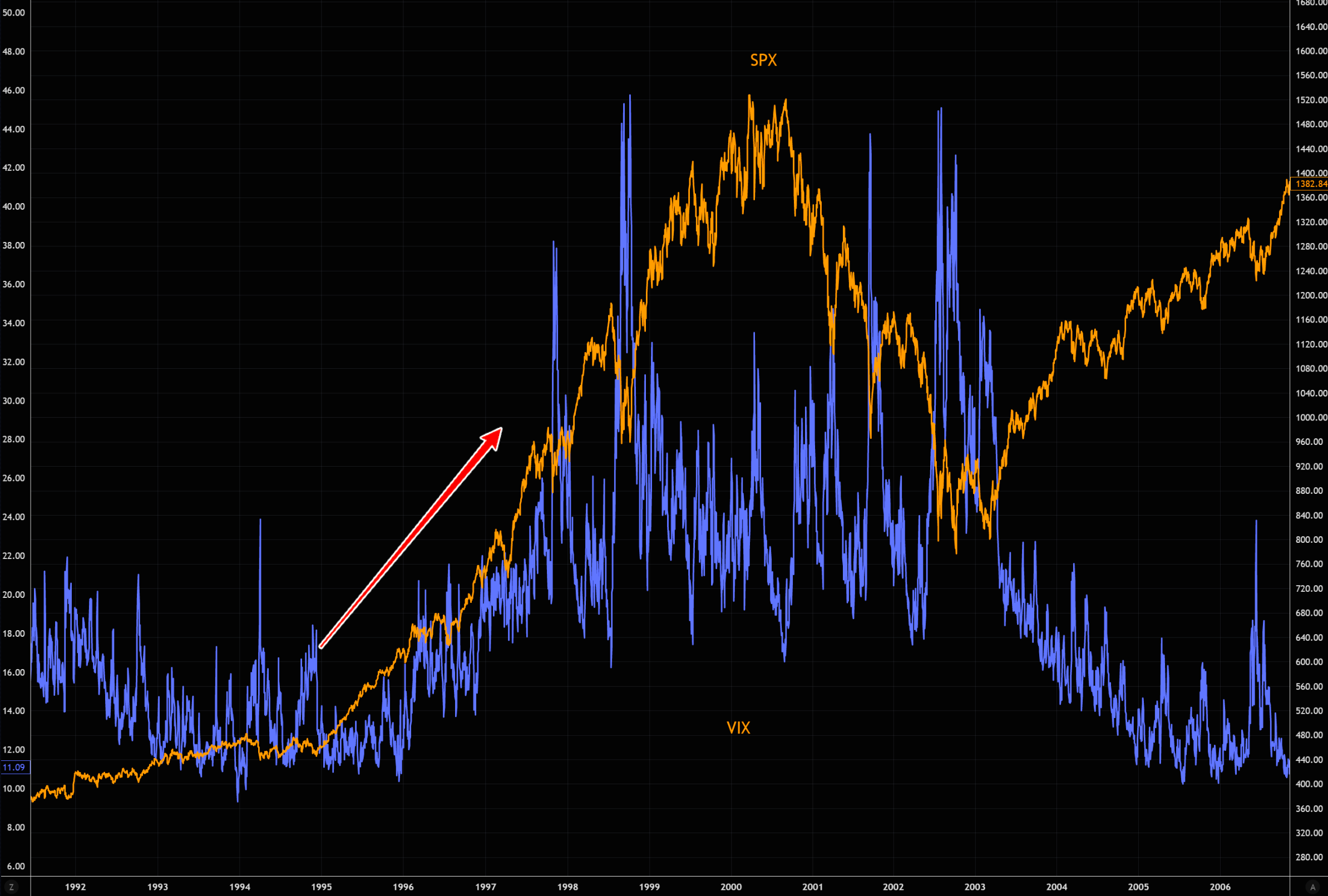

The most extreme "spot up, vol up" regime on record occurred during the latter stages of the 1990s bull market. Demand for upside exposure started building as early as 1996, and volatility gradually shifted into a structurally higher regime.

While the final top was marked by a sharp volatility spike, the underlying repricing of risk had begun years earlier. It ultimately took close to a decade for volatility to fully normalize.

As Tier1Alpha recently noted, SOXL alone generated roughly $12 billion in net rebalancing demand, equivalent to about 45% of its prior-day AUM. That is a staggering number and highlights just how powerful the feedback loops created by leveraged ETFs have become.

This ties in directly with the point we made in our latest leverage note. Leveraged products are no longer a niche corner of the market. They have become a key component of market structure, increasingly influencing flows, volatility, and short-term price action.

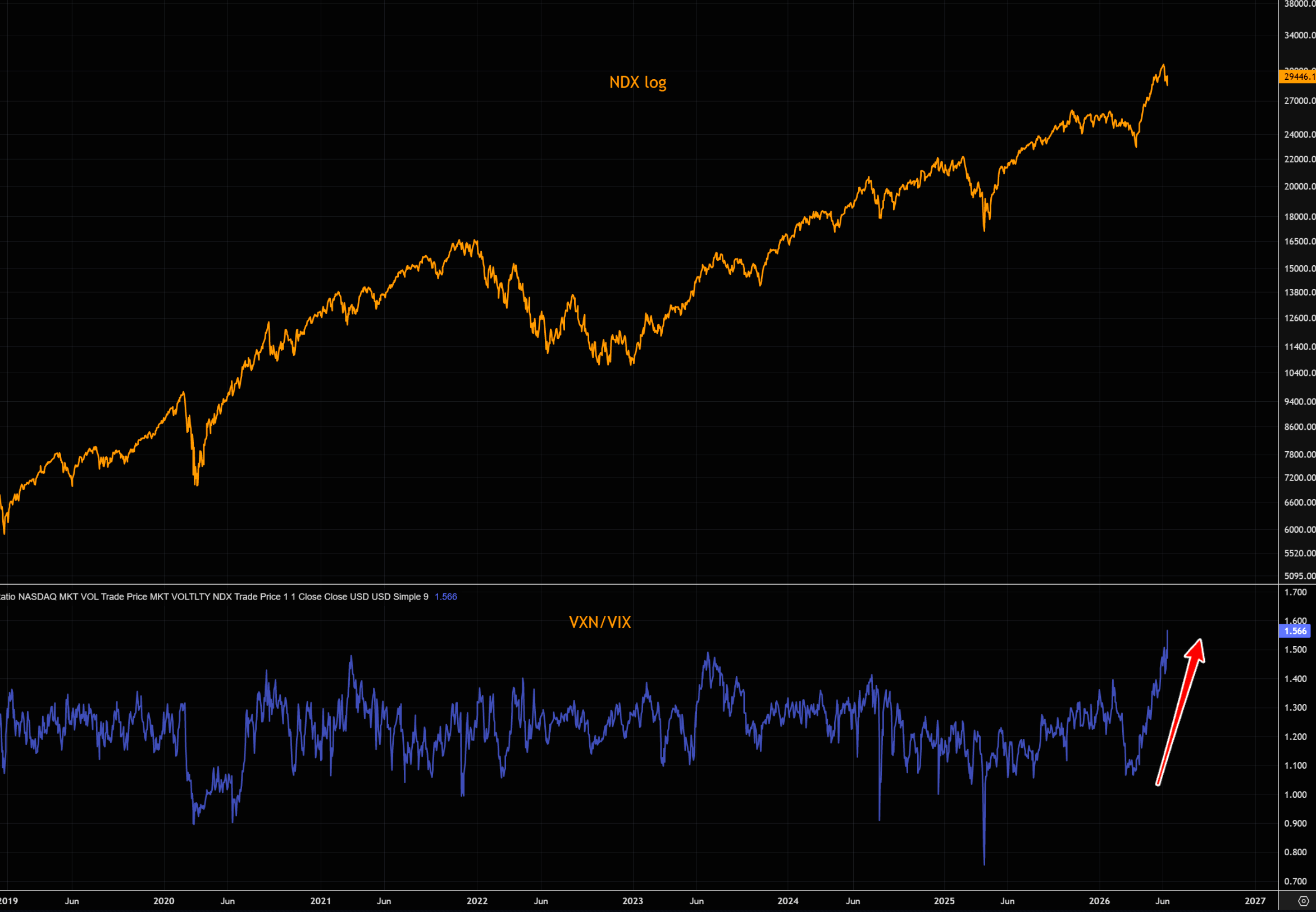

The VXN was introduced after the dot-com bubble burst, which is why we use the VIX for the earlier historical comparisons.

As we have been pointing out for weeks, the recent bid for tech volatility has been extreme. The VXN/VIX ratio has exploded to levels rarely seen outside periods of severe market stress.

This remains a market dominated by technology, and tech volatility is trading at exceptionally elevated levels. Expect more erratic and violent moves in both directions. Latest note on broken markets here.

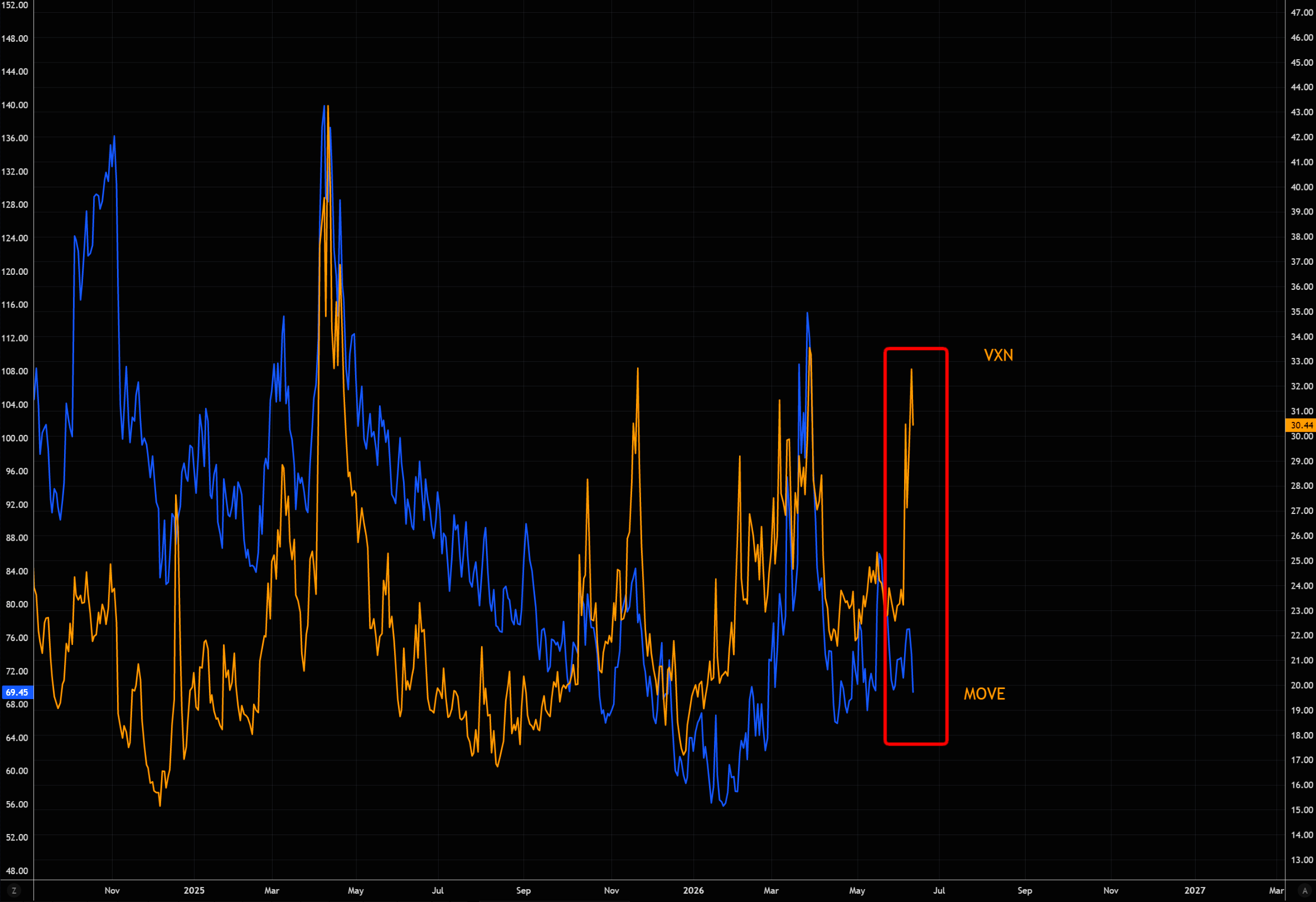

The gap between MOVE and VXN is massive. That makes the divergence even more intriguing given the strong link between technology and rates.

As hyperscalers pour unprecedented amounts into AI infrastructure, big tech is increasingly reverting to a duration trade. The more cash gets shifted from today's balance sheet into tomorrow's earnings potential, the more sensitive valuations become to rates and long-term expectations. More here.

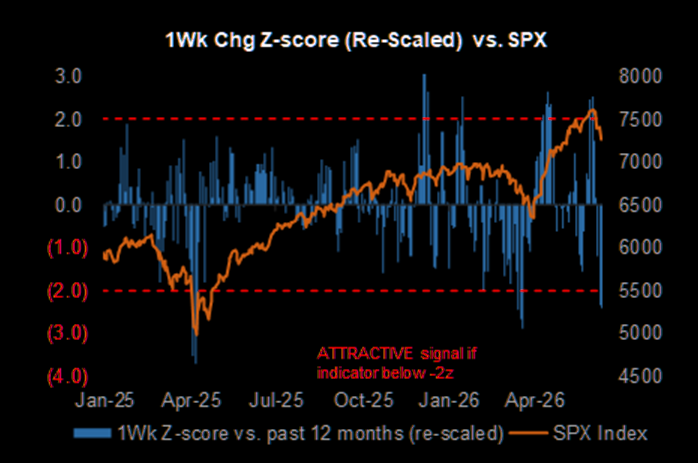

The 1wk change of the TPM flipped aggressively from >+2z at the recent market peak to <-2z this week as positioning level back to neutral… More on the quick de-risk here.

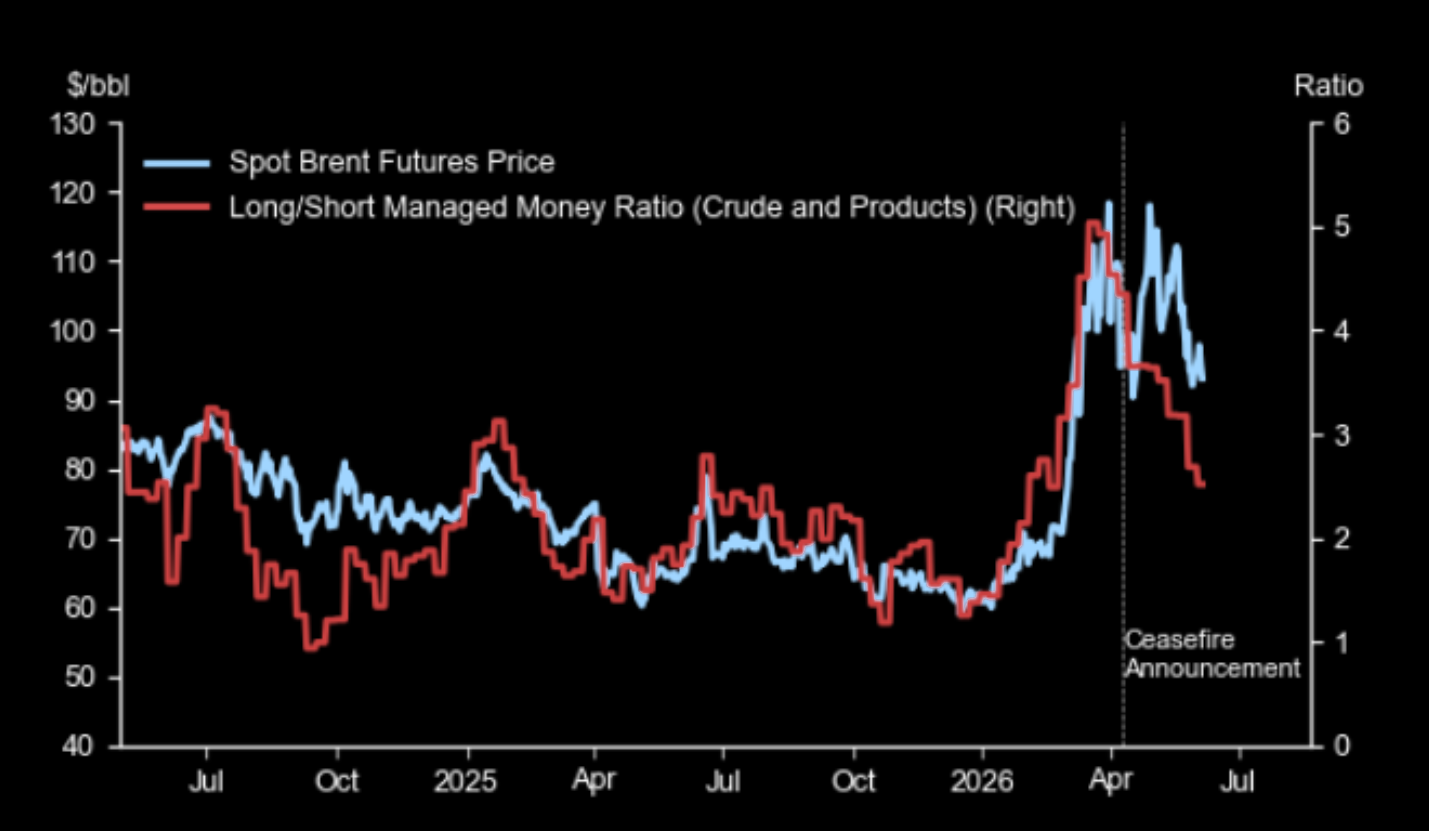

Long/short oil managed money ratio has declined steadily since the ceasefire announcement. More on oil here.

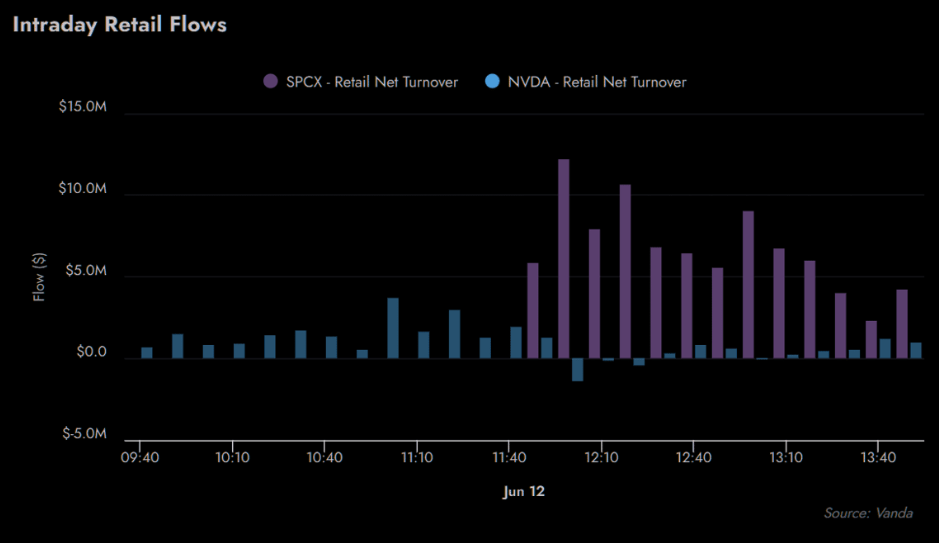

SpaceX - the biggest IPO debut for retail investors, ever (chart several hours before the close). Chart 2 shows just how tiny NVDA suddenly looks.

The scale of retail participation highlights that speculative appetite remains alive despite the recent volatility.