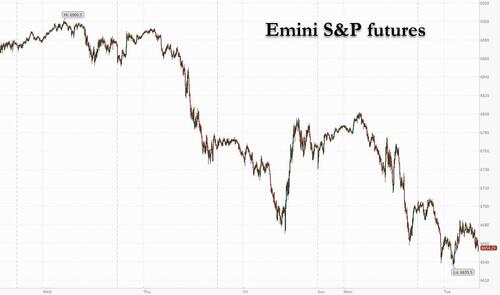

US equity futures are sharply lower again - but off session lows - after the S&P 500 and Nasdaq closed below their 50-day moving averages for the first time since April; both tech and small caps are lagging as the market tries to find a level as the bond market continues to reduce the probability of a further Fed easing. As of 8:00am. S&P futures are -0.6%, set for the longest losing streak since late August. Nasdaq 100 contracts were also -0.6%. Pre-market, Mag7 names are mostly lower with AAPL/GOOG in the green and Semis are weaker. Cyclicals are poised to lag Defensives as the risk-off tone continues. Bitcoin has also pared its drop to 0.4%, having earlier fallen below $90,000 for the first time since April with traders are betting on even more downside. Rotation trades helped to support the overall market last week, but both the Dow and Russell 2000 underperformed yesterday. Topping the list of worries are AI valuations and whether the Fed will cut rates next month. Fund manager positioning (crowded in stocks and low on cash) is also a possible headwind, according to BofA. Treasuries were the main beneficiaries as investors continued to seek havens, with the 10-year yield falling four basis points to 4.09%. Gold fluctuated above $4,000 an ounce. The dollar was little changed. The macro data focus is old Aug / Sep data being released but ultimately the market awaits NVDA and NFP; the Fed Meeting Minutes may give additional color on the Fed’s reaction function into the Dec meeting.

In premarket trading, most Mag 7 names are lower: Microsoft (MSFT) falls 1.5% and Amazon (AMZN) is down 1.8%, underperforming Magnificent Seven peers after Rothschild & Co Redburn downgraded the stocks for the first time since initiating coverage in June 2022. Alphabet Inc. (GOOGL) is up 0.6% after Loop Capital upgraded the Google parent to buy from hold. Apple (AAPL) +0.4%, Meta Platforms (META) -0.7%, Tesla (TSLA) -0.8%, Nvidia (NVDA) -1.1%

Barrick Mining (B) is up 2.5% after the Financial Times reported that Elliott Management has built a “large” stake in the gold miner.Home Depot (HD) falls 3.5% after the retailer reported comparable sales and adjusted EPS for the third quarter that missed the consensus estimates. They also reduced the annual EPS guidance.Honeywell International (HON) falls 2.1% after BofA Global Research cut the recommendation on the industrial giant to underperform from buy, becoming the lone sell-equivalent rating in Bloomberg data. BofA expects shares to lag as elements of its spinoff strategy disappoint investors and the company doesn’t deliver earnings growth next year.Medtronic (MDT) is up 3.5% after the medical device maker lifted the bottom end of its range for adjusted profit forecast for the year.Molina Healthcare (MOH) is up 3.1% after hedge fund manager Michael Burry touted the health insurer in a X post.In corporate news, Apple’s iPhone 17 series drove a 37% rise in its monthly smartphone sales in the key China market, according to Counterpoint Research. Akzo Nobel agreed to acquire smaller rival paint maker Axalta Coating Systems in a €7.9 billion ($9.2 billion) deal. Baidu posted its biggest quarterly revenue slide on record, despite major AI spending.

The ongoing global rout underscored continued unease over interest rates and technology earnings, with Nvidia Corp.’s report on Wednesday poised to test investor nerves over lofty valuations in the artificial-intelligence sector. Focus will then turn to the delayed September jobs report due Thursday, a key gauge for the Federal Reserve’s policy outlook. With all the talk of a potential bubble in AI, most recently with comments from JPMorgan Vice Chairman Daniel Pinto, Nvidia earnings on Wednesday are crucial for market direction. The report “will be the ultimate ‘blue or red pill’ moment for the market,” said Stephan Kemper, chief investment strategist at BNP Paribas Wealth Management. Options suggest an earnings-related move of about 6.4%, roughly matching Nvidia’s recent average, according to data compiled by Bloomberg.

“The question is whether the selloff will continue after Nvidia’s results,” said Eric Bleines, a fund manager at SwissLife Gestion Privée in Paris. “This will make the difference between the market just taking a breather or going for a correction.”

Additionally, traders have less conviction about that, with interest-rate swaps now implying a less-than-50% likelihood of a December rate reduction. Several Fed officials have recently cautioned against a cut, although Governor Waller repeated his view in favor of lowering rates.

“A bit of volatility and a pullback into year-end was on Santa’s wish list for a majority of institutional accounts,” wrote Mohit Kumar, chief economist and strategist for Europe at Jefferies. “Apart from retail investors, we do not think there is a lot of pain on the street.”

Meanwhile, in a sign that US government agencies were resuming operations after the longest shutdown on record, the Labor Department’s website showed 232,000 initial jobless claims for the week ended Oct. 18. Data for the previous three weeks weren’t available. Weekly employment estimates from ADP Research due later Tuesday will offer more insight into the labor market.

Barclays strategists led by Anshul Gupta said Nvidia’s results and the September payrolls report will shape near-term sentiment. They see potential upside for the chipmaker amid accelerating AI investment and rising demand for computing infrastructure, but note the stock has posted negative one-week returns in four of its last five earnings periods.

European stocks followed their Asian counterparts lower, with the Stoxx 600 down 1.3% and looking at a fourth day of losses, with mining and auto shares leading declines, while health care and personal care equities are the biggest outperformers. Here are the biggest movers Tuesday:

Roche shares gain as much as 7% after the drugmaker announced its phase 3 study evaluating investigational giredestrant as an adjuvant endocrine treatment for people with ER-positive, HER2-negative, early-stage breast cancer met its primary endpoint at a pre-planned interim analysisRheinmetall shares rise as much as 4.7% after the German maker of tanks and ammunition said it is targeting sales of about €50 billion in 2030, while also providing guidance around margins and cash conversionImperial Brands climbs as much as 3.2% after reporting its full-year results and outlining guidance for 2026. Panmure Liberum says the tobacco company’s results are on “the right side” of in-lineGreencore Group shares jump as much as 6.7% after the food producer posted earnings ahead of expectationsMining shares are the worst performers in Europe on Tuesday, falling as much as 3.2%, as aluminum and copper declined ahead of publication of delayed US economic dataUK lenders were among the worst-performing banks in Europe on Tuesday amid tax worries ahead of Chancellor of the Exchequer Rachel Reeves’s budget announcement on Nov. 26Umicore shares dropped as much as 14% after a vehicle of holder Groupe Bruxelles Lambert sold roughly €300 million worth of shares in the chemicals company in an overnight placingABB shares drop as much as 4.7%, the most in seven months, after the provider of power and automation technologies updated its financial goals ahead of its capital markets dayCrest Nicholson shares fall as much as 12%, most since August 2024, as the UK housebuilder forecasts full-year profits at the low end of the range analysts expectedEarlier in the session, Asian stocks dropped, poised for a third-straight session of losses, as concerns about an artificial intelligence bubble returned to the fore ahead of Nvidia’s earnings report. The MSCI Asia Pacific Index fell as much as 2.4%, dipping below its 50-day moving average for the first time since April. A sub-gauge of technology shares led a broad decline across all sectors, with chipmakers TSMC and SK Hynix the biggest drags. Most markets in the region were in the red, with gauges in South Korea, Taiwan and Japan down more than 2% each. Concerns of AI overexuberance dominated sentiment as investors awaited Nvidia earnings due Thursday morning in Asia. A filing showed Peter Thiel’s hedge fund sold its entire stake in the chip-maker in the third quarter, adding fuel to market concerns over sector valuations. Tensions between Beijing and Tokyo impacted markets for a second day, with Korean travel shares advancing after China warned its citizens against visiting Japan. Meanwhile, analysts said Philippine stocks could face more headwinds due to political instability as President Ferdinand Marcos reshuffles his cabinet.

In FX, the Bloomberg Dollar Spot Index is little changed with not much movement versus the majors.

In rates, treasuries advance, with US 10-year yields falling 3 bps to 4.10%. UK and German government bonds also rise. Treasury futures hold gains with stock futures lower and technology sector in focus. Focal points of US session include weekly ADP jobs data and three scheduled Fed speakers. Treasury yields are richer by as much as 4bp-5bp in front-end and belly, outperforming long end and steepening the curve; 2s10s spread is about 1bp wider, 5s30s about 2bp; 10-year near 4.10% is about 2bp richer vs German counterpart, about 4bp vs UK. Treasury auctions this week include $16 billion 20-year bonds on Wednesday and $19 billion 10-year TIPS Thursday.

In commodities, spot gold is steady near $4,040/oz. Brent is trading near session highs, around $64.38.

Looking ahead, today's US economic calendar includes ADP weekly jobs data (8:15am), August factory orders (10am) and September TIC flows (4pm); initial jobless claims in the week ended Oct. 18 numbered 232k in data posted to Labor Department website after being delayed by US government shutdown. Fed speaker slate includes Barr (10:30am), Barkin (11am) and Logan (7:55pm) On the corporate side, Home Depot reports earnings.

Market Snapshot

S&P 500 mini -0.6%Nasdaq 100 mini -0.6%Russell 2000 mini -0.7%Stoxx Europe 600 -1.2%DAX -1.2%CAC 40 -1.2%10-year Treasury yield -3 basis points at 4.1%VIX +0.8 points at 23.16Bloomberg Dollar Index little changed at 1220.57euro little changed at $1.1581WTI crude -0.2% at $59.8/barrelTop Overnight News

White House officials are insisting that latest tariff relief doesn't amount to a retreat from the president's staunch defense of tariffs as economic drivers, as critics say the White House is capitulating on its signature economics policy. NBCUS initial jobless claims totaled 232,000 in the week ended Oct. 18, according to US Labor Department website showing historical data. The data’s release had been affected the government shutdown. BBGMark Carney won a key budget vote by the slimmest of margins in Canada’s Parliament, ensuring the survival of his government and avoiding an election. BBGHong Kong bankers and regulators are showing signs of growing concern about the city’s deepest real estate downturn since the Asian financial crisis. BBGChina has bought nearly a million tons of US soybeans, a move that ends a temporary pause and appears to signal commitment to a trade truce agreed late last month. BBGGovernor Kazuo Ueda told Prime Minister Sanae Takaichi that the Bank of Japan is in the process of slowly dialing back its easing support for the economy, signaling his unshaken intention to carefully raise rates. BBGBanking execs in the EU are bracing to be disappointed when officials lay out proposals to cut red tape in the coming weeks, as they predict that the measures will be far behind the deregulation taking place in the US. BBGApple’s iPhone 17 series drove a 37% rise in monthly smartphone sales in China. BBGHome Depot (-3% premkt) cut its full-year earnings guidance, warning that some unsteady consumers are hitting the pause button on big-ticket home purchases. A modest miss was expected. Goldman thinks expectations were for a very small cut and it feels like we could say this was slightly worse than expectations.This earnings season, the share of firms discussing AI-related productivity on earnings calls has been highest within Communication Services and Financials. This quarter, 74% of Comm Services companies and 66% of Financials companies mentioned AI in the context of efficiency on their conference calls. AI-related productivity mentions were lowest in Utilities, Energy, and Materials. GIRJPMorgan COO Pinto says the US economy is not likely to enter a recession. On AI, says, there is likely to be a "correction" in AI valuations at some point. Upside for the S&P from here is relatively limited.US President Trump said he wants 1% inflation: BBG Trade/Tariffs

EU Trade Commissioner Sefcovic says the EU plans to introduce restrictions on EU exports of aluminium scrap.German Finance Minister on rare earths says Germany must do its homework and diversify supply chains.A more detailed look at global markets courtesy of Newquawk

APAC stocks extended losses throughout the session following a similar lead from Wall Street, which had seen heavy losses on Monday. Overall newsflow in APAC hours was quiet, although tech stocks were among the laggards in the region. ASX 200 showed a clear defensive bias across its sectors, with tech the hardest hit. No obvious reaction was seen to the RBA minutes, which largely emphasised uncertainty and data-dependence. Nikkei 225 edged lower after the open and eventually surrendered the 49,000 level, falling as much as 3% intraday. Several additional factors on top of the global risk aversion could've exacerbated losses, including woes surrounding Japan–China relations and the recent JPY and long-end JGB weakness. Several Japanese officials verbally intervened throughout the session but failed to sway the index meaningfully. KOSPI lagged as the index joined the global stock rout, following the prior day's outperformance. Hang Seng and Shanghai Comp opened in the red and initially conformed to regional losses, with Hong Kong underperforming the Mainland amid its tech exposure.

Top Asian News

BoJ Governor Ueda says he discussed the economy, inflation and monetary policy with Japanese PM Takaichi. Will decide on monetary policy while scrutinising various data. FX was discussed, won't comment on details. Desirable for FX to move to reflect fundamentals.Japanese Finance Minister Katayama said she is keeping an eye on markets with regard to fiscal policy and would not comment on FX levels, adding she is alarmed over FX moves; she said currencies should move in a stable manner reflecting fundamentals, and that the government will thoroughly monitor for excessive or disorderly forex fluctuations with a high sense of urgency. She noted concern over recent one-sided, rapid FX moves and said that while GDP avoided the worst, negative growth justifies a sizeable package, according to Reuters.Japan’s Economy Minister Kiuchi said long-term rate moves are determined by markets and that the government is watching market moves — including long-term rates — closely, according to Reuters.RBA November meeting minutes said it is appropriate in the current environment to remain cautious and data-dependent, with members determined they could remain patient while assessing incoming data on the extent of spare capacity. On rates, the minutes noted a mixed picture on whether policy remains restrictive — in contrast with the clearer signals seen in 2024 — and said the cash rate could be held at its current level if demand recovers more strongly than expected, while policy easing is still seen if the labour market weakens materially or growth disappoints; the Board said it is not possible to be confident about which scenario is more likely. The minutes said there may be a little more underlying inflationary pressure than previously assessed, noted the AUD remains close to equilibrium estimates, and said global growth is likely to slow in H2 2025, though the likelihood of a severe downside scenario has diminished, according to Reuters.European bourses (STOXX 600 -1.3%) opened lower across the board, in a continuation of the downbeat mood seen in Wall St and in APAC trade overnight. Indices found a base in early morning trade, where they have resided throughout the morning so far. European sectors are entirely in the red, and hold a clear defensive bias. Healthcare tops the pile, buoyed by strength in Roche (+5.6%), after a positive trial update related to a breast cancer pill. To the downside, Autos, Tech and Basic Resources are all pressured. US equity futures (ES -0.2%, NQ -0.2%, RTY -0.2%) are modestly lower across the board, albeit not to the extent seen in Europe. Traders count down their clocks till NVIDIA earnings on Wednesday, but before that markets will have some US data (Durable Goods, Weekly ADP Average Estimate) and a couple of Fed speakers. Earlier, a surprise jobless claims release (w/e 18th Oct) had little impact on contracts.

Top European News

EU Commission says definitive measures imposed consist of country-specific tariff rate quotas per type of ferroalloy, limiting the volume of imports to enter the EU duty free.FX

DXY is currently choppy and trades within a busy 99.39 to 99.60 range. Initial action saw the index buoyed by the downbeat risk tone, where the USD was pressured by typical haven currencies such as the JPY & CHF whilst the Antipodeans lagged. Thereafter, the risk tone improved a touch and the Dollar dipped to make a session low – a move which also came amidst a surprise US weekly claims release. Do note that the weekly claims release is a delayed report for the w/e Oct 18th; it printed at 232k, whilst continuing claims printed at 1.957mln. Looking ahead, ADP will release its weekly US jobs gauge; last week, it reported that its average weekly estimate was -11,250. US factory orders are expected to have risen by 1.4% M/M in August (prev. -1.3%); durable goods revisions for August are also due today. NAHB's housing market index is seen unchanged at 37 in November. Fed's Barr (voter) and Fed's Barkin (2027 voter) are set to speak, while Fed's Logan (2026 voter) will deliver remarks after the close.EUR is currently flat/mildly lower and largely moving at the whim of the Dollar given the lack of pertinent European newsflow. Initially flat vs the Dollar, then caught a bid to make a fresh session high above the 1.1600 mark – before once again reversing. Bid seemingly in the moments preceding the US jobless claims figures. Currently towards lows at 1.1583.JPY is also flat vs the USD, but began the European session a little firmer, having benefited from the subdued risk tone seen overnight. That downbeat sentiment has remained this morning, with equities continuing to reside firmly in the red – albeit have stabilised just off worst levels. For Japan specifically, a number of key sticking points; 1) a meeting between BoJ Governor Ueda and PM Takaichi, 2) China-Japan tensions, 3) ongoing verbal intervention.GBP is steady vs the USD, but as above, was subject to some two-way action surrounding the US jobless claims data. Currently trading in a 1.3146 to 1.3176 range. Focus for the day will be on commentary from BoE's Pill and Dhingra this afternoon, and then will shift to the UK's inflation report on Wednesday. A dataset which has heightened focused, given BoE Governor Bailey highlighted inflation developments at the most recent confab - he is likely to be the deciding vote ahead in December; markets currently assign a 79% chance of a 25bps reduction at that meeting. More pertinent for the GBP are budget-related updates. Most recently, The Telegraph reported that UK Chancellor Reeves is reportedly considering a last-minute raid on banking profits in the budget. This would be a politically favourable move, but perhaps overshadowed by the growth-related implications of such a move, and boost concerns re. the UK’s investment attractiveness.Antipodeans were initially the clear underperformers vs the USD overnight and into the European morning – though as the session progressed, that move has since stabilised. AUD is essentially flat and trades within a 0.6466 to 0.6499 range whilst the Kiwi is marginally firmer and trades within a 0.5639 to 0.5669 range.Fixed Income

USTs started the day on a firmer footing, buoyed by the risk tone, and have continued to grind higher as the morning progressed. USTs at a 112-19 peak, posting gains of nine ticks at most. Eclipsing Monday’s 112-24+ best but stopping just shy of a cluster from last week between 113-01+ to 113-04+. Upside this morning was also spurred by a surprise release from the Department of Labour, jobless claims at 232k in the October 18th week and continuing at 1.957mln (prev. 1.947mln); no direct comparison to initial, the last release was 219k for the week of September 20th. Notably, the move in US fixed income assets to the release was fairly muted in nature. Potentially a function of participants awaiting more timely series and/or the hard data to begin to be released in the next few days and weeks before reassessing their position in December. Ahead, we get the latest ADP series (not the BLS reference period), a handful of other prints and remarks from Fed’s Barr (voter) and Barkin (2026) on supervision and the economic outlook respectively.Bunds are bid, in-fitting with the above. Lifted across the early European morning before seeing a bit of a pullback just after the cash equity open and in proximity to the time of the discussed US jobless claims series. A pullback that was possibly a function of cash equity benchmarks opening slightly better than futures had implied at their worst and/or participants being caught off guard by the DOL release. Since, Bunds have resumed their climb and are towards highs of 128.90 as the European tone remains subdued overall and the fixed income complex generally moves higher.Gilts are also moving alongside peers. Currently at the top-end of a 92.41 to 92.60 bound. Specifics for the UK light today, as we count down to Wednesday’s CPI release for confirmation that inflation has peaked and early insight into the December meeting. UK specifics remain focused on the budget, and while there have been a handful of pertinent updates, primarily relating to domestic banking names, nothing has emerged to significantly change the narrative for rates at this point in time.UK sells GBP 1.25bln 4.75% 2030 Gilt by tender: b/c 3.75x, average yield 3.896%China began marketing a EUR bond sale to raise up to EUR 4bln; guidance was set at mid-swaps +28bps for the 4-year tranche and mid-swaps +38bps for the 7-year tranche, according to Bloomberg and the term sheet.Commodities

Crude benchmarks initially sold off during the APAC session as risk sentiment continued to sour but has pared back on earlier losses at the start of the European session. WTI and Brent dipped to a trough of 59.28/bbl and 63.62/bbl respectively before reversing higher to peak at 59.73/bbl and 64.07/bbl. Benchmarks currently continue to trade towards session highs, to make a fresh peak at USD 59.91/bbl and USD 64.25/bbl, for WTI and Brent respectively.Spot XAU has steadied above USD 4k/oz as the metal continues to struggle to act as a traditional safe haven during US equity selloffs. XAU fell throughout the APAC session from the open at USD 4044/oz to a trough of USD 4004/oz as the European session got underway. The yellow metal briefly dipped below US 4k/oz to a low of 3998/oz before attracting buyers that took price c. USD 45/oz higher to a high of USD 4042/oz as US data got released.Base metals have continued to drop, following the broader risk aversion. 3M LME Copper opened at USD 10.76k/t and gradually fell c. USD 100/t to a trough of USD 10.66k/t. The red metal has managed to find a base at these levels and currently, 3M LME Copper is trading in tight c. USD 70/t band at the lows of the day.Rio Tinto (RIO AT/RIO LN) reduced production at its Yawun alumina refinery to extend its operational life, with output set to decline by 1.2mln tonnes annually and the refinery’s production to be cut by 40% in 2026, according to Reuters.Goldman Sachs says as global LNG supply continues to rise faster than Asia demand, estimates that NW European storage will face congestion in 2028/29 which would pressure TTF and JKM low enough to reduce global LNG supply.Commerzbank expects copper and aluminium to reach USD 12,000/t and USD 3,200/t respectively in 2026. Zinc prices to settle around USD 3,000/t. Nickel prices to settle at USD 16,000/t.Geopolitics: Middle East

The UN Security Council adopted the US-led resolution establishing an international stabilisation force in Gaza, with 13 countries voting in favour while Russia and China abstained, according to Reuters.Hamas said the UN resolution imposes international trusteeship on Gaza, which is rejected by Palestinians and factions, and that the resolution does not meet Palestinian rights and demands, according to Reuters.US President Trump said the US will be selling F-35s (LMT) to Saudi Arabia.Geopolitics: Ukraine

A White House official said President Trump would sign the Russia-sanctions bill if decision-making authority remains, according to Reuters.The US Treasury said sanctions against Rosneft and Lukoil are reducing Russian oil revenues and pushing Russian crude prices to multi-year lows, while Treasury OFAC analysis stated the sanctions may have a long-term negative effect on the volume of Russian oil sales.The Ukrainian military said a Russian missile attack targeted the east of the country, according to Al Arabiya.Ukraine's President Zelenskiy announces plans to go to Turkey on Wednesday to reinvigorate negotiationsGeopolitics: Others

Japan’s Trade Minister Akazawa said there are currently no particular changes in China’s export-control measures on rare earths and other products, according to Reuters.North Korea said South Korea’s nuclear-propelled submarine will lead it to arm itself with nuclear weapons and said it will respond to the confrontational stance of the US–South Korea joint factsheet, via KCNA.The US Ambassador to Japan posted that the United States is fully committed to the defence of Japan, including the Senkaku Islands, and said nothing the China Coast Guard flotilla does can change that fact, via X.US Event Calendar

10:00 am: Nov NAHB Housing Market Index, est. 37, prior 3710:00 am: Aug Factory Orders, est. 1.4%, prior -1.3%10:00 am: Aug F Durable Goods Orders, est. 2.9%, prior 2.9%10:00 am: Aug F Durables Ex Transportation, est. 0.4%, prior 0.4%10:00 am: Aug F Cap Goods Orders Nondef Ex Air, est. 0.59%, prior 0.6%10:00 am: Aug F Cap Goods Ship Nondef Ex Air, prior -0.3%4:00 pm: Sep Total Net TIC Flows4:00 pm: Sep Net Long-term TIC FlowsCentral Bank Speakers

10:30 am: Fed’s Barr Speaks on Bank Supervision at American University11:00 am: Fed’s Barkin Speaks on the Economic Outlook7:55 pm: Fed’s Logan Delivers Closing Remarks at ConferenceDB's Jim Reid concludes the overnight wrap

It’s been a challenging start to the week as markets brace for two key events: Nvidia’s earnings tomorrow night and the US payrolls report on Thursday. I'm old enough to remember when the US employment report came once a month on a Friday! For now, equities remain under pressure, with the S&P 500 (-0.92%) posting a third consecutive loss for the first time since September and marking its worst three-day run since April (-2.61%) with futures down another half a percent as I type this morning. Concerns swirling around the AI trade pushed Nvidia (-1.88%) to another decline, US HY spreads widened (+5bps), and the VIX index (+2.55pts) closed at a 4-week high of 22.38pts. And there was no respite from the slump in crypto, where Bitcoin (-3.32%) fell to its lowest level since April with another couple of percent of declines seen this morning. It's now down around -4% in 2025 and nearly 30% of its YTD peaks 6 weeks ago.

Those losses for the S&P 500 brought the index below its 50-day moving average, often viewed as an important technical threshold, for the first time in 139 sessions. That was the longest such run since 2007. While AI weakness was a key driver, sending the Philadelphia Semiconductor Index -1.55% lower, it was a day of broad weakness with 407 decliners within the S&P 500, the most in 5 weeks. The small cap Russell 2000 (-1.96%) and the equal-weighted S&P 500 (-1.31%) both fell to their lowest levels since August. The Mag-7 (-0.08%) actually had a better day but this was mostly thanks to Alphabet +(3.11%) which rallied on news that Berkshire Hathaway took a stake in the company last quarter. Credit spreads ticked a little higher, with US IG and HY spreads +1bps and +5bps wider respectively. Those moves came as Amazon became the latest of the tech giants to tap the bond market, raising $15bn in its first bond offering in three years.

In addition to the AI concerns, the risk-off tone was reinforced by the latest signals from the Fed, as investors continued to price out the likelihood of a December rate cut. Futures now imply just a 41% probability, down from 43% on Friday – with the highest rate priced for the December contract since late August. This hawkish tilt has been evident since Powell’s October press conference, and front-end Treasury yields reflected that, with the 2yr yield (+0.3bps) rising to 3.61% even as the risk-off tone brought 10yr yields lower (-0.9bps to 4.14%). However, the continued risk-off move overnight has helped 2yr and 10yr yields to rally -3.1bps and -2.3bps respectively.

The reason the front-end initially held up was partly driven by a surprisingly strong Empire State manufacturing survey from the NY Fed yesterday. Normally a second-tier release, it grabbed attention given the lingering data backlog from the shutdown. The headline index surged to 18.7 in November (vs. 5.8 expected), its highest in a year, reinforcing the view that the US economy has held up well and the Fed needn’t rush into further cuts.

The ongoing decline in December cut expectations came despite slightly dovish remarks from Vice Chair Jefferson, who saw the “balance of risks in the economy as having shifted in recent months with increased downside risks to employment compared to the upside risks to inflation, which have likely declined somewhat recently”. That said, he left December open as a data dependent decision. More clearly on the dovish side of the FOMC, we heard from Fed Governor Waller, who repeated the view that the Fed should cut rate again in December, saying that this would “provide additional insurance against an acceleration in the weakening of the labor market”.

The sell-off is continuing overnight with the KOSPI (-3.06%) leading the declines, with the Nikkei (-2.90%) not far behind. Japanese long-bonds continue to sell-off as markets fear a larger-than-expected supplementary budget later this week from the new Takaichi administration. The 40yr bond has hit its highest level, +8bps to 3.68% this morning, with the 30yr is +5.1bps.

Elsewhere, the S&P/ASX 200 (-1.94%) is also seeing large losses after the minutes from the RBA’s November meeting indicated that the central bank remains largely cautious regarding further interest rate cuts. Meanwhile, the Hang Seng (-1.55%) is also trading noticeably lower, with the Shanghai Composite (-0.50%) outperforming. S&P 500 (-0.45%) and NASDAQ 100 (-0.55%) futures are off their session lows but are still declining.

In Europe yesterday, the market moves largely echoed those across the Atlantic, as the STOXX 600 (-0.54%), DAX (-1.20%) and CAC 40 (-0.63%) all posted a third consecutive decline. Futures are showing further declines of around a percent overnight. European bonds matched Treasuries, with yields on 10yr bunds (-0.8bps), OATs (-0.6bps) and BTPs (-2.6bps) all slipping. 10yr Gilts rebounded more (-3.9bps) after a tough Friday session. The European Commission published its autumn forecasts. Growth for the Euro Area in 2025 was revised up to +1.3% (from +0.9%), while 2026 was trimmed to +1.2% (from +1.4%). Inflation forecasts were steady at +2.1% for 2025, but nudged up to +1.9% for 2026.

In reality, the news flow was light yesterday. Canada’s October CPI was mixed: median core CPI eased to +2.9% (vs. +3.0% expected), but headline CPI edged up to +2.2% (vs. +2.1%). A December cut by the Bank of Canada was already seen as unlikely, but the odds fell further to just 3%, from 6% before the weekend.

Looking ahead, today brings comments from Fed officials Barr, Barkin and Logan, alongside the BoE’s Pill and Dhingra. On the corporate side, Home Depot reports earnings.

Loading recommendations...