Report: Obamacare Fraud Is Worse Than You Think

Following the expiration of the Covid-era enhanced Obamacare subsidies at the end of last year, the corporate media have remained focused on how much Exchange enrollment might decline this year. But a new report issued by the Department of Health and Human Services (HHS) provides another perspective on the issue.

Official reports by the Congressional Budget Office and Government Accountability Office have previously examined how applicants misstate their income to qualify for subsidies and how Exchanges permitted enrollment of fictitious applicants. But the data HHS analyzed gives additional context and granular details surrounding improper enrollments into Exchange coverage. It provides yet another reminder that “success” should not merely consist of the number of people (real or otherwise) enrolled in government programs — and that Congress and the administration should take additional action to guard against fraud.

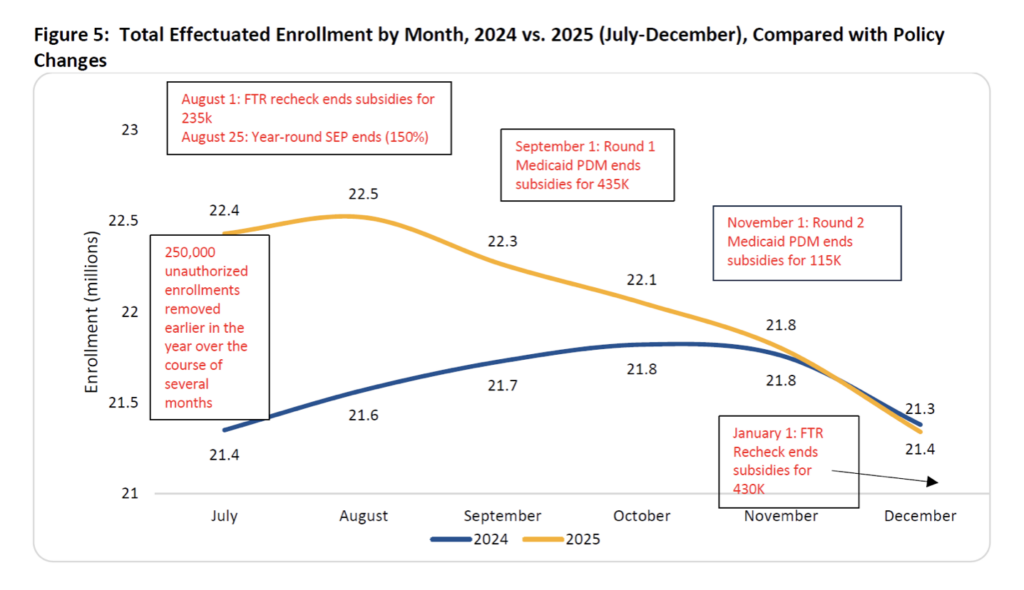

Individuals RemovedThe report shows two facets of the same story: groups of individuals who have been disenrolled over the past year and additional groups still enrolled who show signs of questionable activity. The report reveals how the Centers for Medicare and Medicaid Services (CMS) removed enrollees over the second half of last year due to various program integrity efforts.

As the graphic below shows, two rounds of Medicaid periodic data matching (PDM in the chart) — i.e., removing people enrolled simultaneously in Medicaid and Exchange subsidies — culled the rolls by about 550,000. Likewise, CMS also removed approximately 665,000 enrollees who did not file federal taxes to reconcile the subsidies they received in prior years (which are based on projected income) with the subsidy amounts they should have received based on actual income (i.e., failure to reconcile, or FTR in the chart).

Additionally, the report notes that “27.8 percent of individuals in a plan where they pay no premiums whatsoever have canceled their plans through May 2026.” It would ordinarily make no sense for someone receiving “free” health coverage to disenroll from it — unless of course they were enrolled without their consent or are concerned about having to repay subsidies they do not qualify for.

The corporate media have focused on the 4 million decline in enrollment — i.e., the difference between the 23.1 million people who selected a plan during open enrollment (which ended in January) and the 19.2 million that the report says are paying premiums and currently enrolled. But if large percentages of people are canceling “free” coverage, that is a separate story in and of itself.

Continued Questionable ConductThe report notes other potential flags that may indicate questionable enrollments of individuals who remain covered in Exchange plans. For instance, “CMS recently identified 1 million highly suspicious agent and broker assisted enrollments through Healthcare.gov with no social security number on their application who are also paying no premium.”

CMS would also like to remove an additional 300,000 people from subsidies for failing to file tax returns and therefore not reconciling their subsidy amounts for prior years. However, a federal judge has prohibited the administration from enforcing a rule issued last year that would require subsidy recipients to file taxes and reconcile past subsidies every year (as opposed to every two years under a Biden-era policy).

Questionable Value of CoverageFinally, the report notes that more than half (55 percent) of enrollees who were in a zero-premium plan last year, but were enrolled in a plan that required a premium in 2026, had their enrollment canceled for failure to pay that premium. By contrast, from 2017-2022, only an average of 18 percent of enrollees had their plan canceled for not paying a premium after being enrolled in a zero-premium plan the prior year.

The growth in the rate of individuals getting coverage canceled when faced with a premium could reflect improper enrollment. However, it could also mean that some enrollees just don’t value their coverage. They will stay signed up when the coverage is “free” (i.e., totally paid for by the federal government) but will drop their plan if required to pay even a nominal premium.

Recall that a Brookings Institution study last year found that charging enrollees a de minimis premium of even $1 per month would cause nearly 1 million individuals to drop coverage. As I noted at the time, most Democrats would view this as a bug because people might become uninsured. But some conservatives might consider requiring everyone to pay something for their health coverage a feature, while asking a related question: If almost a million Americans won’t even pay $1 monthly to enroll in an Exchange plan, what does that say about how they perceive the value (or lack thereof) of Obamacare?

Affordability DebateI won’t attempt to argue that the enhanced subsidies’ expiration had no effect. Near-retirees and households just above 400 percent of the poverty level (who became ineligible for subsidies) may face a substantial change in their out-of-pocket monthly costs for insurance.

But the numerous signs of improper enrollment outlined in last week’s report — to say nothing of the myriad ones that preceded it — coupled with the federal government’s $39 trillion in debt, argue against spending another $350 billion (plus interest) to extend the enhanced subsidies. With fraud rampant and government spending stoking the rise in health care costs, such a measure would have only made both problems worse.

Chris Jacobs is founder and CEO of Juniper Research Group and author of the book "The Case Against Single Payer." He is on Twitter: @chrisjacobsHC.